Weekly Random Walk - 5/8/2026

Tenzing Norgay

Tenzing Norgay

Tenzing Norgay was a Nepalese Indian Sherpa mountaineer. He ascended with Sir Edmund Hillary as the first confirmed person to ever summit Mount Everest as part of the 1953 British Mount Everest expedition. Tenzing reached the top of Everest without supplemental oxygen (a feat few humans have accomplished). Time magazine named Norgay one of the 100 most influential people of the 20th century.

In 1953, Norgay took part in John Hunt’s expedition; Tenzing had previously been to Everest six times (and Hunt three). A member of the team was Edmund Hillary, who fell into a crevasse but was saved from hitting the bottom by Norgay’s prompt action in securing the rope with his ice axe, which led Hillary to consider Norgay his climbing partner of choice for any future summit attempt.

On May 29th, 1953, Hillary and Norgay made their attempt to summit but faced a 40-foot rock face later named “Hillary Step,” in which they wedged their way up the crack face between the rock wall and ice face. Once they overcame that obstacle, the rest of the effort was relatively simple. They reached Everest’s 29,028-foot summit, the highest point on earth, at 11:30 am. They spent only about 15 minutes at the summit before starting their descent back to the base camp. Hillary said many times that without Norgay’s guidance, he would never have been able to crest the summit.

The job of a Tibetan Sherpa is to guide. To provide the climber with all of the tools and direction to be successful. As we looked at this week’s markets and conversations with clients (BW), we realized that our job is “Sherpa-like” in assessing and navigating these high-climbing equity markets and economic data.

We hope this week we lead you to some clarity and keep you from danger.

The risks of the ascent

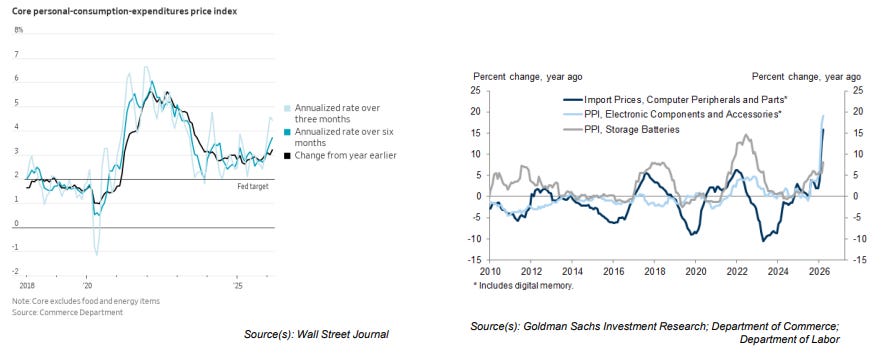

We have consistently highlighted the issue of inflation over the last few months, but it was nice to see the Fed also identify the stickiness of higher prices. The quote in the headlines from Fed Chair Powell at last week’s FOMC meeting press conference shows (left chart below) that Core PCE inflation is now running 3.2% year-over-year, but recent momentum is considerably higher, with the three-month annualized rate at 4.5% and the six-month annualized rate closing in on 4%.

Much of the Fed’s dovish inflation view has hinged on fading goods inflation driven by tariffs. Higher gas and diesel prices haven’t yet crept into PCE or CPI, as there is generally a three-month lag. Once those prices move into the data, along with lingering tariff inflation, the Fed has a real issue on its hands, as on one side, they are going to have to deal with higher prices (which normally means rate hikes), while the new Fed Chairman and President Trump want to push Fed Funds lower.

One area where consumers have seen their discretionary spending reduced is due to healthcare costs. There has been double-digit inflation for those needing healthcare insurance, and with high deductibles in most of these policies, consumers are effectively uninsured.

The government has decided not to subsidize insurers, which will likely lead to higher prices, and last week, the Cigna Group, one of the country’s largest health services and insurance firms, joined others, including Aetna and United Healthcare, in divesting its individual health exchange business.

In their press release, Cigna said, “By the end of 2026, Cigna Group will no longer offer insurance through the Affordable Care Act (ACA).” According to their earnings report, as of March 31, the company plans to displace 369,000 members currently on an individual or family plan.

“We did not make this decision lightly, and appreciate the importance of ensuring patients have continuity through the transition,” Brian Evanko, Cigna’s Group president, said during the earnings call. “Looking into the future, there’s no question that the status quo in healthcare is unsustainable. Cost continues to rise, as does demand for healthcare services, an untenable equation,” he said.

Yet, there is nothing coming from Washington to solve the mess they made, and we think there is a high probability that healthcare inflation could accelerate to the point where lower- and middle-class families are put under enormous financial stress beyond where they are today.

The fixed ropes, are they secure?

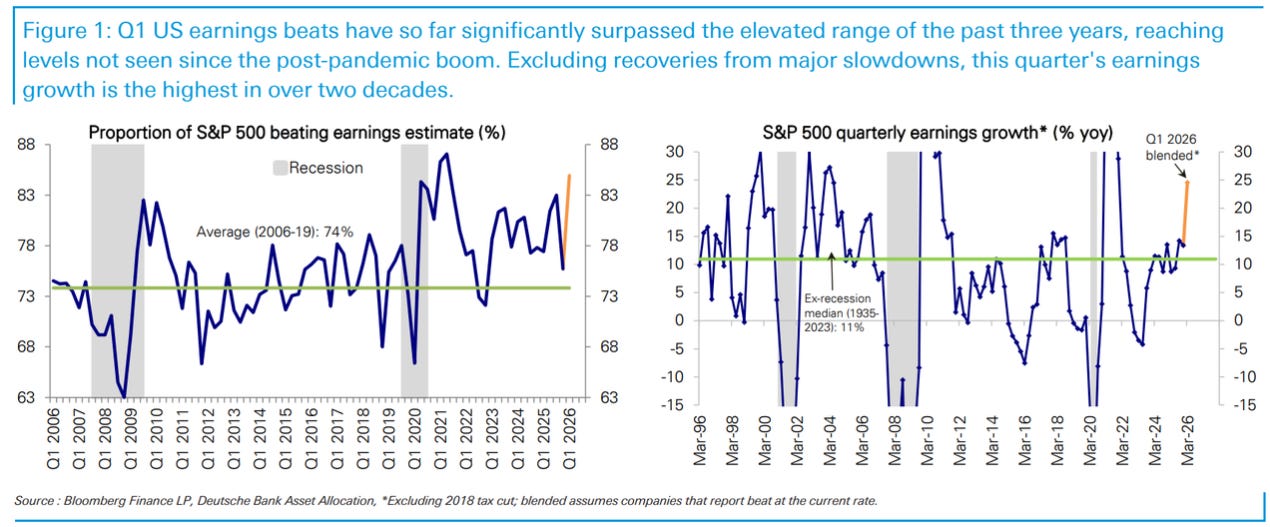

Despite geopolitical risks, markets continue to rise, and one key reason is the remarkable US Q1 earnings season. Earnings are significantly exceeding consensus estimates across all metrics despite a high bar.

S&P 500 earnings growth is projected to accelerate sharply from 13.4% in Q4 to 24.6% in Q1 – a four-year high and a level rarely seen outside of post-shock recoveries (example: COVID). Excluding special factors, this represents arguably the strongest growth in decades.

The AI boom is a clear contributor, but its impact is widespread, with double-digit growth across average and median companies, and all 11 sectors posting positive growth for the first time in four years. The strong performance has been driven by higher prices amid supply constraints, surging demand in the AI value chain, and other disruptions.

In light of these results, Deutsche Bank has raised its 2026 EPS forecast from $320 to $342, driven by strong Q1 beats, gravity-defying performance in MCG & Tech, and higher oil and commodity prices.

But like a Sherpa keeping climbers from complacency, we continue to navigate markets with caution. We admit the AI capex narrative is lifting stocks despite what we think will be global economic problems stemming from our war with Iran. There is a feedback loop in AI that has created momentum in this market, which, if we are honest, has surprised our estimates.

However, as higher stock prices support spending by the wealthy, the more resilient consumers look – even if it reinforces the K-shaped economy (haves and have-nots) and masks shaky confidence as lower-income households are hurt more by higher costs.

Also, there is a danger that US growth becomes overly dependent on the investment cycle of a single new technology. If the capex momentum wavers, power becomes too scarce or AI delivers the feared labor-market shock, the optimistic part of the feedback loop breaks. In that scenario, the risk, however distant, is that the rally destroys itself.

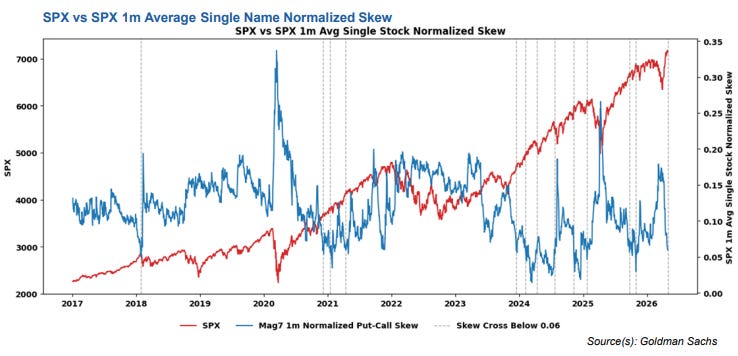

We continue to see complacency across various market segments, including the options market. The SPX has continued to move away from the Put-Call skew as the fear of missing out on the rally has pushed SPX higher. This type of divergence and spread is often followed by bouts of volatility and deviation in equity markets.

So, as markets climb higher, we suggest continuing to watch your step.

Altitude sickness – consumers are out of oxygen

If you are earning the same amount as in 2020, you are in a much worse financial position today. As a result, people are more concerned about the economy than anything else. According to Gallup, the percentage of Americans who believe that their finances are getting worse has been rising for five years in a row and is now at the highest level EVER recorded.

Americans’ financial outlook in 2026 is historically poor, with a record 55% now saying their financial situation is getting worse. While similar to last year’s 53%, this is up from 47% in 2024 and marks the fifth consecutive year in which more Americans say their finances are worsening than improving.

Majorities worry about not having enough money for retirement (62%) and being able to cover medical costs in the event of a serious accident or illness (60%). Slightly smaller majorities (54%) worry about their investment returns and maintaining their standard of living.

What is more disturbing is that, on average, it takes only a little over $6,000 in additional debt to push a family over the edge. In a country that just flew astronauts around the moon, mapped the human genome, fights in endless wars, and produces more billionaires per capita than any other place on this planet, this seems to be unacceptable.

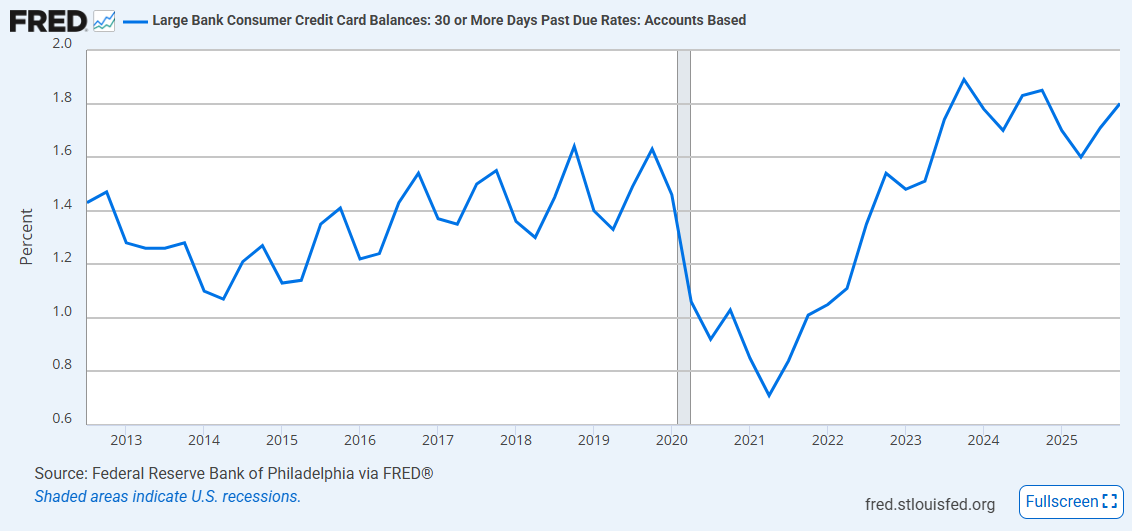

You can see consumer stress below, as large bank consumer credit card balances of 30 days or more are close to all-time highs. This Federal Reserve Bank chart covers Q4 2025, and we anticipate surpassing the 2024 highs when Q1 is reported.

The financial stress on ordinary Americans doesn’t stay financial for long; it often then evolves into political stress. It would seem counterintuitive for lawmakers to hit stressed consumers with dozens of taxes and fees unless local, state, and federal spending are out of control. Depending on where you live, middle-class consumers can pay up to 50% of their income in taxes and fees. They work until June just to pay their taxes. We understand how extreme parts of the political spectrum (Democratic Socialism and MAGA) are dominating our parties today. Frustration with lawmakers is at an all-time high (and their favorability at an all-time low). This had made it easy for extremes in the party to gain momentum and actually make things worse. This is like the Khumbu Icefall on the ascent of Everest (known as the most technically dangerous section of the route). If lawmakers don’t start moving to the middle of their parties to solve US problems, we could see the system collapse like the ice blocks at the Icefall.

Rates keep climbing

Treasury yields continue to rise and are approaching key levels, as the long end of the yield curve is pushing them to uncomfortable levels. As you see below, the 10-year (as of 11 am EST on Friday) is trading at a 4.36%, breaking out of a large triangle formation. A push a bit higher from here, say the 4.50% level, and things would get messy quickly (chart source: Market Ear). In mountaineering terms, these are like altitude markers that can guide you technically when to buy or sell.

The 30-year has been bouncing around the 5% level (currently at 4.94%). This seems to be a resistance point; however, if we saw a continued sell-off and a close below 5.1%, it would push it into uncharted territory (chart source: Market Ear).

Readers of this report know we have stayed at the shorter end of the yield curve with our bond purchases. If these resistance levels are broken, we would begin to extend the duration of our portfolios as real return levels become attractive. We continue to look at Investment Grade, Agency, Municipal, and Treasury bonds.

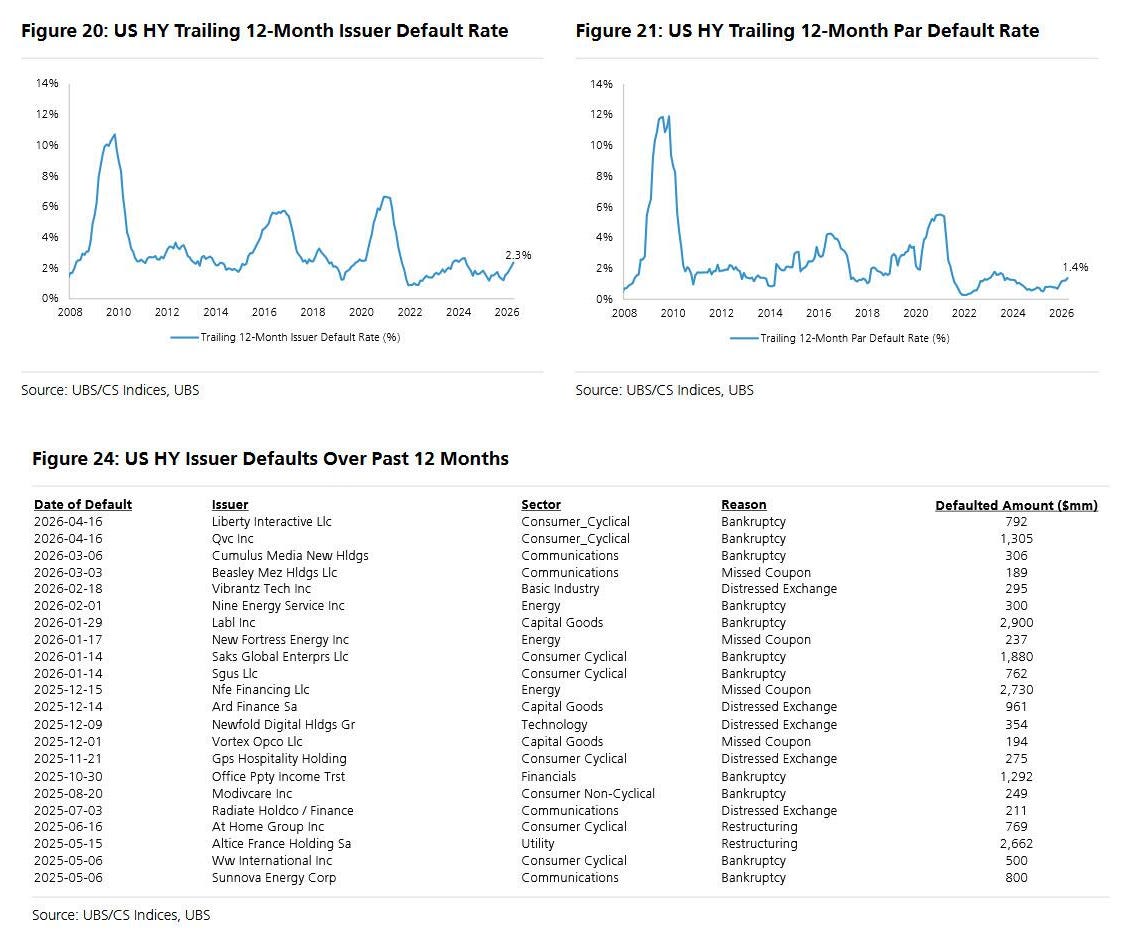

We have stayed away from high-yield (junk) and private credit as we continue to agree with various analysts like Matt Mish of UBS, who two months ago sparked a mini-crisis on Wall Street when he predicted private credit default rates of 15% (in his April Default Report). Last week, he updated his research, highlighting that the private credit market picture remains clouded as the liquidity crunch in funds managed by Blue Owl, Blackstone, and BlackRock added to the sector’s complexity.

The report on high-yield credit was also downbeat and not because default rates have more than doubled (2.3% LTM, up from 1.1% a year ago) but because other key aspects of cumulative losses/recoveries unexpectedly plunged to 35% from 51% a year ago, prompting concerns about underlying unsecured asset quality. This means that if a company defaults, high-yield managers can capture only 35 cents on the dollar invested, versus 51 cents or 16 cents of additional loss.

If AI stubs its toe or the economy goes into recession (a lot of “ifs” there), we anticipate loss numbers to increase and high-yield spreads to widen dramatically. Hence, our rationale for staying in the IG (investment-grade) paper.

First to summit

Lastly, Larry Fink, who oversees $11.5 trillion at BlackRock, spoke at the Milken Institute Global Conference and said six words that are profound: “We just don’t have enough compute.”

“The US is short of power. We’re short on compute. We’re short chips. And there’s going to be shortages in all three of memory, four things. I actually believe a new asset class will be buying futures of compute.” In essence, Fink is predicting that computing will become a tradable commodity like oil, grain, or natural gas, with forward contracts on future capacity arising from structural, predictable shortages, so that a derivatives market will emerge to price and trade them.

The numbers behind Fink’s six words are staggering, as data centers will consume 70% of all memory chips produced globally in 2026. Advanced HBM production from Samsung, SK Hynix, Micron, and Nvidia is all sold out through 2026 and through a large part of 2027. DRAM supply growth is running at just 16% annually, while AI infrastructure demand is growing at 80%.

Despite geopolitical chaos, economic slowdowns, consumers on the brink, the equity market is looking at one thing and one thing only…the race for computing power. We are six weeks into this rally, and it appears the S&P 500 will hit all-time highs. As we have highlighted this week, several factors could derail this ascent, but our job in this report is to ensure you understand the risks and provide enough information to keep your asset climbing. Like Norgay, the Vito Report doesn’t claim to reach the summit first. We just try to make sure you get there – and back – in one piece. Until next week, watch your step.

Trade well.

VR

This commentary is for the Vito Report only. The opinions represented in this piece are those of TVR and not of any affiliated companies. This research is based on current public informaton that we consider reliable, but we present it as accurate and complete, and it should not be relied on as such. The information, opinions, estimates, and forecasts included here are as of the date hereof and are subject to change without prior notice. We would like to update our commentary as appropriate. Some commentary can and will be published irregularly as applicable in the analyst’s judgement.

This research is not an offer to sell or solicitation of an offer to buy security or service in any jurisdiction where such an offer or solicitation would be illegal. It does not constitute a personal recommendation or take into account ZPW clients’ particular investment objectives, financial situations, or needs. Readers should consider whether any advice or guidance in this research suits their specific circumstances and, if appropriate, seek professional advice, including financial and tax. Past performance is not a guide for future performance. Any investment has risks and potential loss of capital. Invest wisely.